08 — Our Story

Started by financial services professionals who had seen the problem from the inside.

Started by financial services professionals, we came together — six of us initially. We decided there had to be a better way. For years we had worked inside big banks and finance companies, desperately trying to make a difference but confounded by inefficiencies, blockers, and poor leadership.

All of us had spent our careers trying to make an impact — to help the customers, to help our co-workers, to provide strategy and direction from our experience. Despite the inertia of big banks to improve, to change, to genuinely lift their customers' experience, we did independently make gains. We did make things better. But there had to be a better way. How could we really make a difference?

Independently we made gains, but what could we achieve outside the constraints of the banking monoliths? We realised that across the six of us we had over 200 years of financial experience, and had worked in more than 20 countries. And that was just the immediate founders, not even including the people and contacts that we would inevitably bring in. This was a formidable team.

And what about the customer? Internationally, customers are dissatisfied with their big banks. Polls consistently show they would like to change, but unless they're remortgaging, they don't. Why not? Because what's the point — the public perceives all the big banks as being the same.

And what about the smaller banks, the credit unions, the mutuals, the building societies? Their customers really like them. Customer service matters to these organisations, and customer loyalty is the result. But bit by bit, they're disappearing. It's very hard to compete with banks with huge technology budgets. Governance and regulatory requirements put a huge burden on smaller institutions. One by one they've been merging to survive, or having to close. These are companies with histories that go back hundreds of years, and to see that history and legacy vanish is a horrible result. Certainly not good for the end consumer.

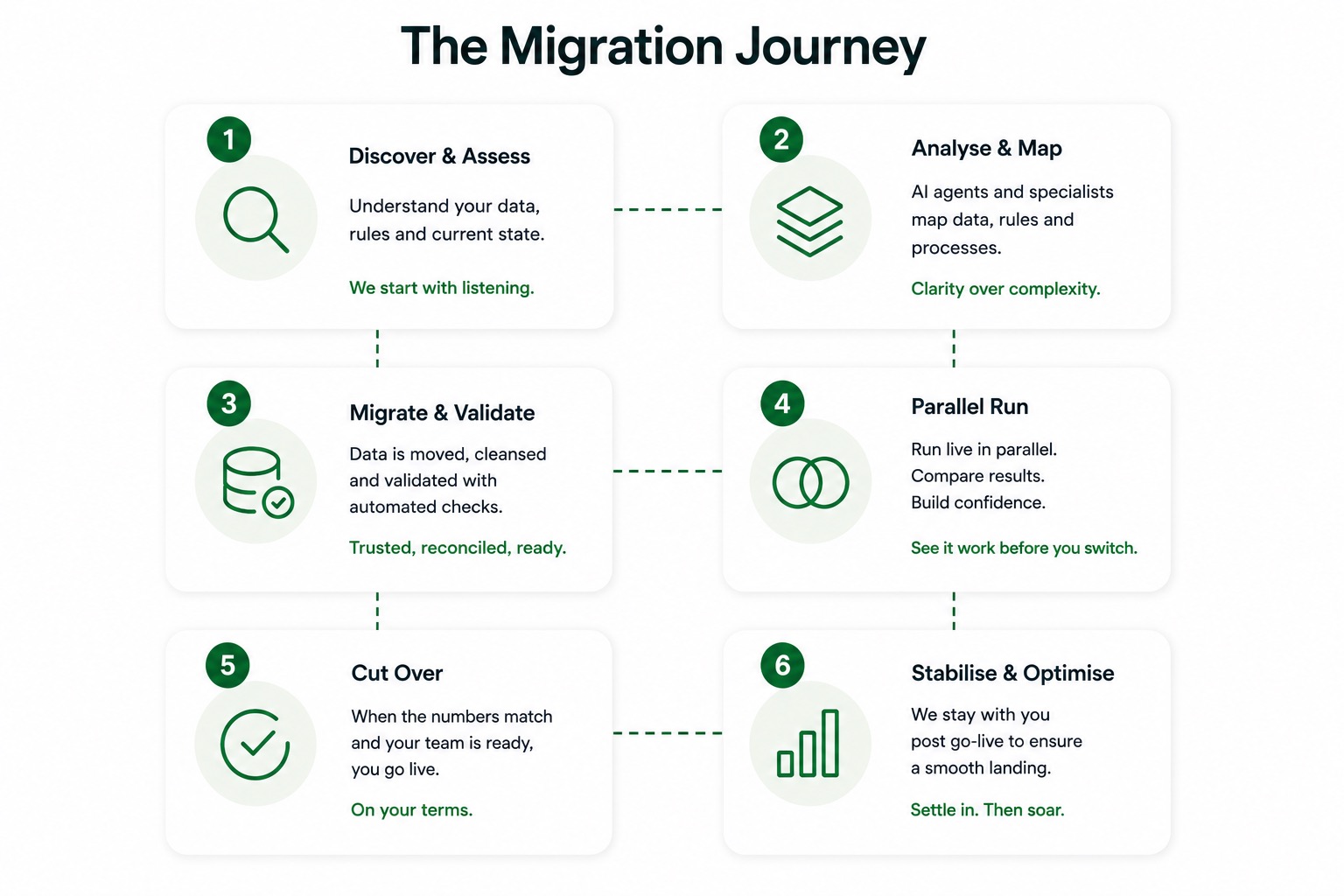

Hence Totara came to be. A modern banking platform with full capability. A modern banking app with a great customer experience. Governance and regulation built in. Simple, scalable pricing. A migration solution built in. The sum of these gives a smaller financial services company another option — other than merging, folding, or a slow attrition of customers.

Customers deserve better than they've been getting from the big banks. Why not give the smaller financial services companies better tools and systems than the big banks have themselves?